When it comes to commercial lending, credit analysis is an essential part of the process. Banks use it to assesses the ability of a business to sustain a certain level of debt and repay its loan. A bank can only lend money if it understands the viability of the business and therefore the risk of potentially not being repaid.

This process involves a combination of skill and human judgement and has always encountered difficulty in comparing one business to another. A steakhouse on Wall Street catering to investment bankers, will be nothing like a vegan restaurant in Greenwich Village, even if the two happen to be in the same area. Their clientele, their offerings, their pricing model, and how they respond to different economic stresses, will vary significantly. This is compounded by the fact that veganism wasn’t a popular concept until very recently so there is very little comparable data on the sector available. This lack of data is ironic given that we are inundated on all fronts by data - much of which is difficult to digest and make sense of.

Credit analysis therefore faces three related challenges:

- How to find all the data required to answer a credit question

- How to make sense of this data - given both the volume of data that exists and the gaps in that data - and derive insights from it

- How to apply these insights to understand a business and answer specific credit questions about it

Unless these challenges are met head-on, credit analysts can end up spending the vast majority of their time trying to find data and massage it into a useable format, rather than actually doing analysis. They therefore risk missing crucial insights in the deluge of data points and producing analysis that is weak and not grounded in facts, or worse still, is hampered by their own biases and not applicable to a changing world.

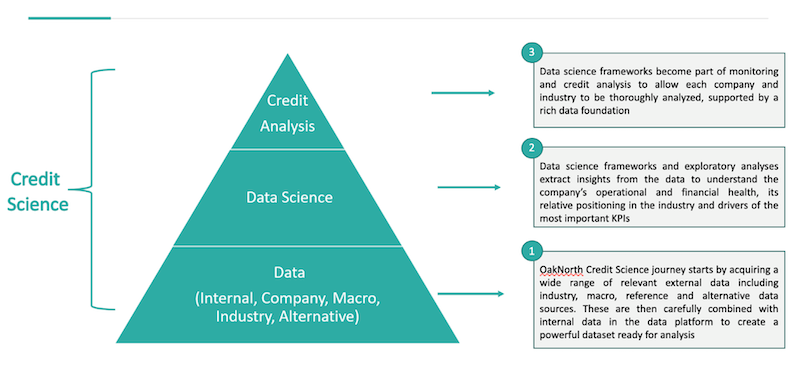

At OakNorth, we’ve created a framework to tackle these challenges, known as “OakNorth Credit Intelligence”:

The foundation of the pyramid is data. We are constantly looking for additional data sources to enhance our understanding and just as importantly, for ways to connect these data sources together to form an intelligible whole. We combine data from numerous sources into a common data lake which can be used to benefit the bank partners using the OakNorth Credit Intelligence Suite, whilst ensuring their data is fully confidential.

We build on this with the use of data science, which derives insights from this data in a robust and scientific manner:

- We construct predictive models to forecast future performance of companies.

- We use clustering to group companies and find outliers.

- We look for drivers - leading indicators which might help us foresee when a particular company or even a whole sector may run into difficulties.

- We use data science to join the dots between data sources, filling in the blind spots using inference and deduction so the picture of a business that emerges is much more focused and filtered than anything available in a single source.

The fact is that commercial lending hasn’t changed for decades – banks are still using the same methods and data sources they used in the 80s, despite the fact that the world has moved on. The internet for example brought with it social media, online reviews, lower sales and distribution costs, new revenue streams, etc. As a result of climate change, consumers are becoming more conscious of purchasing goods and services from businesses that conduct themselves in an environmentally and socially-conscious way.

Think for example if a bank received a loan application from a vegan restaurant in New York City looking for £1.5m of debt finance to open another site. While the bank should of course use financial and operations data to help it assess credit risk, there will be other data sources that should be considered – especially as there’s unlikely to be many other vegan restaurants to compare it to. The location will be key – i.e. it wouldn’t make sense to open it in the middle of the meat packing district(!), the demographic of the surrounding population will also matter as the concept will likely appeal to “millennials” more than older generations, seasonal fluctuations due to trends like “Veganuary” could lead to spikes in popularity, whether the restaurant has an Instagram account to promote its menu and reviews could also impact customer footfall, etc. So, it’s important for multiple data sources – including what may be unconventional or previously unavailable – to be leveraged, as this is the only way we can paint a full picture.

We call the people on our team who are able to combine the disciplines of credit analysis, data science and all the data available – the three layers of the pyramid - “OakNorth Credit Scientists”. Through leveraging the OakNorth Credit Intelligence Suite, we are able to help bank partners make better lending decisions (even when it comes to the types of businesses who may not have existed a decade ago), and more effectively address the needs of the “Missing Middle” – the growth businesses who are the backbones of economies globally but who have been banking’s blind spot for decades.