On August 16, 2024, ONCI hosted a webinar focused on physical risk in commercial real estate (CRE) portfolios, tools for assessing it, and implications for banks. We were incredibly fortunate to welcome Eric Wischman, Climate Risk Officer at M&T Bank and the cover feature of the latest issue of ONside, as a guest speaker, sharing his learnings and insights from his climate risk journey to date.

We were joined in the audience by commercial banking leaders from 15 banks, with combined assets of $3tn. The wide-ranging discussion yielded several interesting insights which we’ve summarised below.Overview

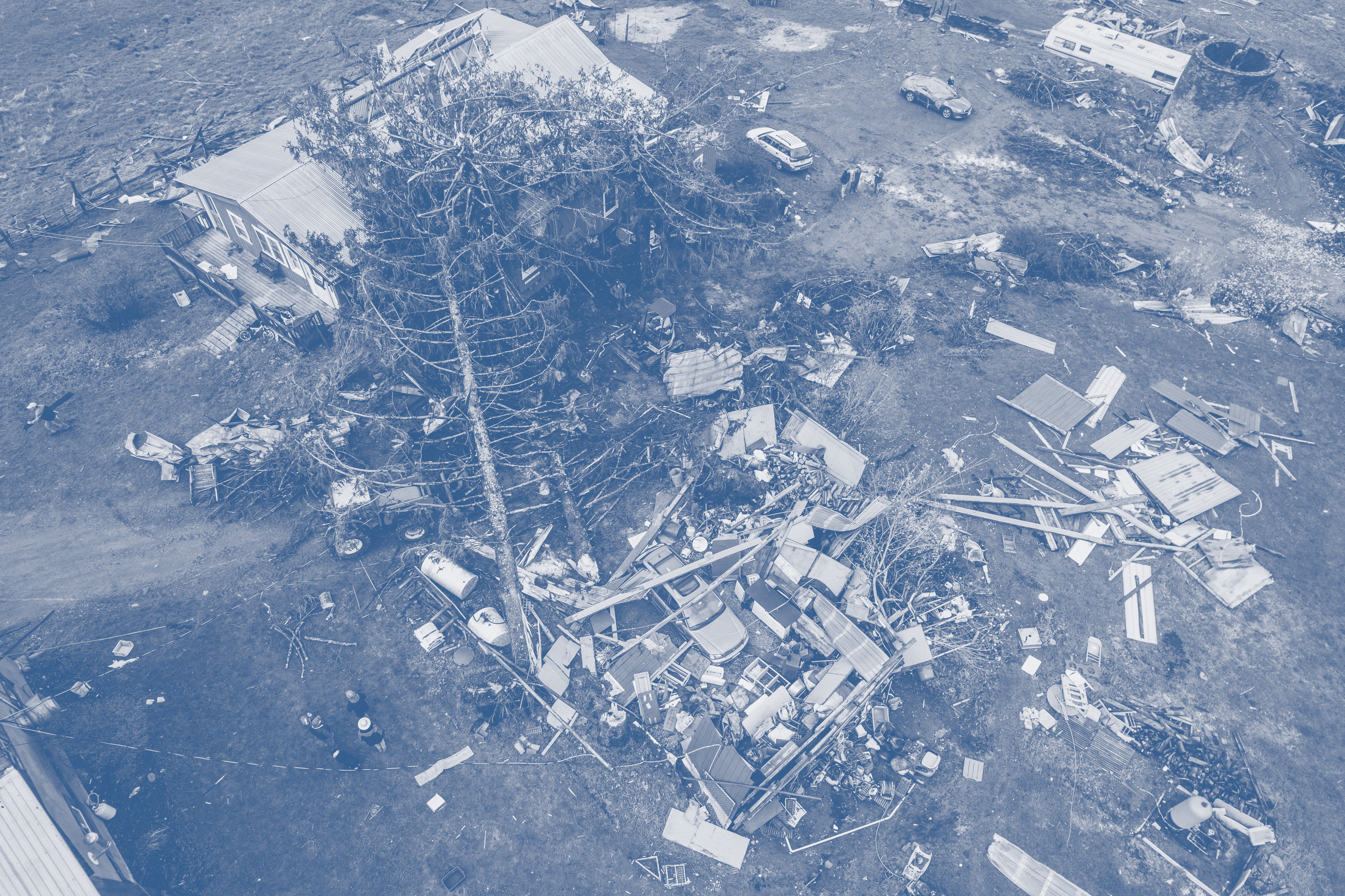

In 2023, there were 28 extreme weather events in the US that caused more than $1bn in damage, and combined, they accounted for almost $93bn in damage. So far, this year in the US, there have been 15 extreme weather events that caused more than $1bn in damage, with a combined cost of $38bn in damage.Events such as these are driving up insurance premiums and repair costs, as well as impacting businesses’ ability to get insurance in the first place. As a result, physical risk management has become an increasing area of focus for both national – the Fed, the OCC, and the FDIC – and state-level regulators in places such as California, New York, and Minnesota. It is perhaps unsurprising therefore that for 80% of the banks who joined the webinar, regulatory scrutiny is the leading driver for them conducting physical risk assessments, followed closely by credit loss evaluation.

It was clear from our conversations that commercial banks are at varying stages of their climate risk journeys. The focus for many has been on gathering and organizing their data, establishing governance, and running Climate Scenario Analysis (CSA) to identify key risk areas. Some are beginning to incorporate CSA outputs into their operations, including credit risk management and strategic planning, as well as initializing conversations with some borrowers.

Data utilization and limitations

Eric shared how M&T Bank started its physical risk management work with data that was public and readily available – FEMA data – and compared that to its lending portfolio across all zip codes. This gave the organization an initial view of where it was more likely to have concentration risk around certain types of physical events.While databases such as FEMA can be a good starting point to get a sense of where high-risk areas have been historically, there are limitations to this given every extreme weather event is different. Just because an event caused a certain amount of damage in the past, it doesn’t mean it would happen in the future with the same degree of impact. FEMA data provides a useful baseline for assessing physical risk, but often lacks geospatial specificity and forward-looking insights. So, supplementing this with forward looking financial impact of perils from partners such as ONCI can help commercial banks make more informed decisions about lending and risk management, particularly in regions facing where extreme weather events are more frequent.

Eric shared how his team spent significant time cleaning up existing internal data, ensuring for example that the address they had on file was the actual address of the collateral, was correctly spelled and had the correct postcode, so that they weren’t measuring risk in the wrong location. Such an exercise can often reveal that a bank’s collateral and lending footprint is more geographically dispersed than initially thought. While certain regions may be well-known for climate risks, other areas also face emerging threats that need to be addressed through proactive risk management and proper insurance coverage. ONCI’s engagement with clients always begins with a review of data quality and advice for addressing data gaps or data quality issues.

Once banks get their data to a good place, they can begin to conduct CSA, and identify the riskier areas within their CRE portfolio, aiding in internal education, reporting, and strategic planning. These outputs can also support origination, credit analysis, portfolio monitoring, strategic planning, and customer engagement. However, he warned that trying to model risk out 20, 30, 40, etc. years will risk engagement from internal business partners, so instead, commercial banking leaders should try to use that data to map out what the bank’s next nine quarters might look like.

Internal culture and communication

Engaging a large organization on climate risk requires careful communication, acknowledging biases, and emphasizing the material risks involved. Eric shared how it's incumbent upon all commercial banking leaders to try and meet people where they are on this particular topic given how polarizing and politicized it can often be. Eric’s approach has never been to try and prove anything to anyone other than the fact that extreme weather events may pose a material emerging risk to the institution. As a large institution, they have a responsibility to try to understand this risk better from a safety and soundness perspective.M&T established a climate risk working group that periodically gathers and shares information with respect to what it’s doing across the organization from a climate standpoint. It's something that M&T leads as part of the second line of defense, overseeing the implementation and integration of climate risk across the organization.

Short-term vs long-term strategies

For CRE construction projects with short time horizons (2-3 years), it's challenging for organizations to align these with the longer-term nature of climate risk which may span decades. Addressing this disconnect is essential for managing both immediate and future risks such as insurance coverage. With insurance becoming harder to secure in high-risk areas (e.g. parts of Louisiana and Florida), banks are adjusting their credit and underwriting policies. It's critical to stay ahead of things like insurance trends, which can be supported by leveraging relationships with insurance carriers for insights into market shifts.Another significant challenge is balancing transaction-level risks with portfolio-level concerns. These parallel paths require using the same data but tailoring insights for both micro-level (individual loans) and macro-level (portfolio) perspectives.

Proactive vs reactive approaches to risk management

Eric noted how risk management has always felt fairly reactive – “you’re always running to the next problem, the next issue, the next loss” – but it should really be proactive, and climate risk management creates the opportunity to do this. This isn’t about looking into a crystal ball trying to predict when or where the next extreme weather event will occur, but more about operational resiliency and preparedness.Given the unpredictability of climate-related events and the complexities of data sourcing and quality, being proactive just in case something happens, as opposed to being reactive and hoping to address it just in time is advised. As noted earlier, regulatory scrutiny is one of the primary drivers of change, and the balance between regulatory pressure ("the stick") and internal business needs ("the carrot") is key to effective proactive risk management.

How ONCI works with customers on their climate journey

ONCI Climate Solution aligns with the Physical Risk module of the Federal Reserve’s CSA guidelines released in January 2023. The Fed CSA’s Physical Risk module focuses on measuring the impact of acute physical risks on large banking organizations’ real estate portfolios. ONCI translates and quantifies the financial impact related to physical risk into actionable outputs such as:- Revenue: Impacted by operational downtime and cost pass-through

- Property Valuation: Estimated damage to property caused by extreme weather events

- Operating Costs: Affected by changes in insurance premiums, downtime, and other costs

- Capital Expenditures: Affected by damages and insurance coverage availability

- Debt: Driven by capital expenditure required to repair physical damage

- Insurance: Impact of physical risk with rising premiums vs absence of insurance